For more stories like this, sign up for the PLANADVISERdash daily newsletter.

Data & Research April 29, 2014

Another Quarter of 401(k) Balance Growth

New analysis from Fidelity Investments shows the

average balance of its client’s 401(k) accounts reached $88,600 during the

first quarter of 2014, boosted by automatic plan features and strong markets.

Reported by

John Manganaro

This represents a 9% increase from $80,900 one year earlier, Fidelity says, and a gain of 92% over the five years since the first quarter of 2009—the market low of the economic downturn—when the average was $46,200. For pre-retirees age 55 and older, the average balance is $165,000, Fidelity says.

“It’s encouraging to see such positive savings results for millions of Americans in the five years since the market downturn, both in 401(k)s and IRAs,” says Julia McCarthy, executive vice president of workplace investing at Fidelity. “But even with this quarter’s positive news, there is still more that can be done to improve outcomes in retirement.”

Overall, still only about one in four (26%) employers automatically enroll employees in their retirement plan. And even for plans with auto-enrollment features, getting more employees to start contributing isn’t always enough to improve plan outcomes. The numbers suggest employers must also take action to help workers save more, Fidelity says.

Fidelity’s average employee deferral rate is 8%, yet for those who were auto-enrolled into a 401(k) plan, the average deferral rate is only 5%. This is in part because 73% of employers with automatic enrollment onboard employees at 3% of annual income or less, so even with an average employer match contribution of 4.4%, the savings rate for many auto-enrolled employees still falls below Fidelity’s recommended annual total savings rate of 10% to 15%.

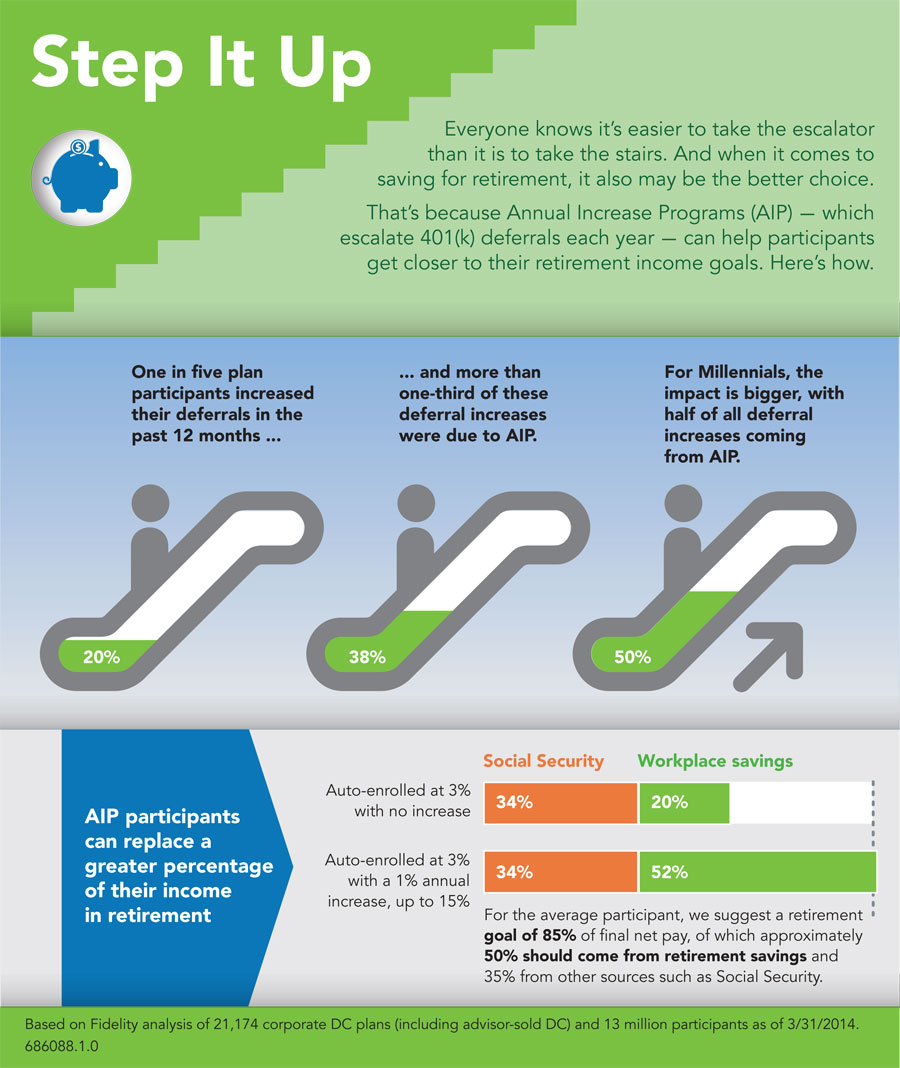

Fidelity says annual increase programs (AIP), also referred to as auto-escalation features, can be powerful tools to help employers have a positive impact on their employee’s retirement readiness. AIPs typically increase deferrals by 1% per year to automatically raise an employee’s total savings to the desired rate.

Fidelity’s data shows that, over the last year, about 20% of employees increased their personal savings rate—the highest percentage since Fidelity started tracking the number seven years ago. Nearly two in five (38%) deferral increases were due to auto-escalation, and of Fidelity’s Generation Y employees, half of all deferral increases were due to such features.

Some form of AIP is offered by 77% of Fidelity 401(k) plan sponsors, but only 12% of this group uses truly automatic escalation features under which employees must actively choose not to automatically increase their contributions annually. With only 7% of employees opting out of Fidelity plans once automatically enrolled, Fidelity says the data is clear that employers can help drive savings rates even higher by incorporating auto-escalation into their auto-enrollment process.

“We understand that saving for retirement competes with numerous financial goals such as the purchase of a home, college tuition and the escalating costs of health care in retirement,” says McCarthy. “Fidelity recommends companies offer automatic features to promote participation and annual savings increases by employees. And we urge investors to take advantage of additional savings opportunities such as individual retirement accounts (IRAs) and health savings accounts (HSAs), if available, to help build their individualized retirement paycheck.”

Fidelity says the first quarter 401(k) data again underscores the positive impact financial advice and education can have in helping employees make informed decisions about their retirement savings and investment strategies. In 2013 Fidelity noted a 42% increase in guidance sessions, and of those employees who consulted with a financial adviser, 37% took a positive action, such as increasing the savings rate or reviewing asset allocations.

An infographic depicting the role AIP plays in boosting retirement savings can be downloaded here. The quarterly 401(k) update is available here.

{kind=link}