For more stories like this, sign up for the PLANADVISERdash daily newsletter.

Data & Research May 27, 2021

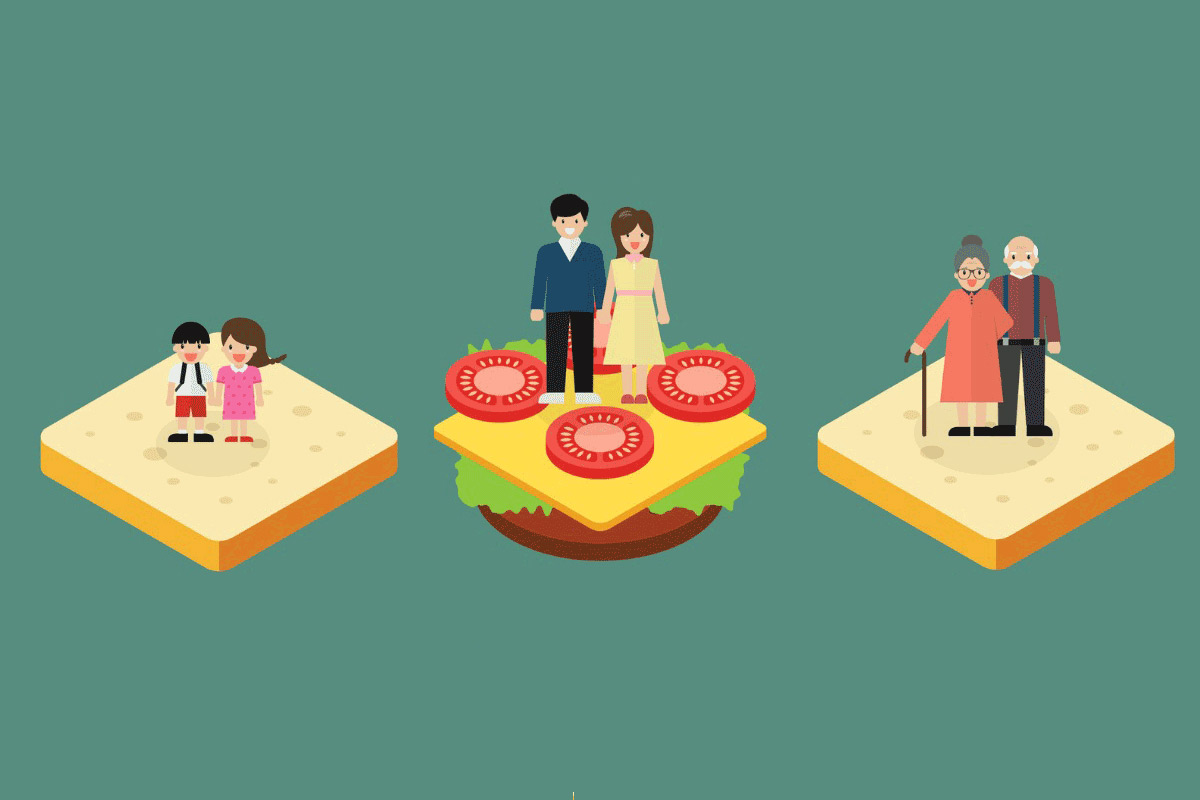

Gen X Participants Are Even More ‘Sandwiched’ After COVID-19

However, there are several helpful actions and concepts that advisers can bring to the table.

Reported by

Lee Barney

While one might expect Baby Boomers, as the oldest generation in the workforce, to have been more materially impacted by the COVID-19 pandemic in terms of layoffs, furloughs and pay cuts, surveys have found the generation right after Boomers, Generation X—or roughly those between the ages of 41 and 56—was harder hit. Millennials and younger adults suffered the most job disruptions.

According to a report from Greenwald Research and the Society of Actuaries, “Financial Perspectives on Aging and Retirement Across the Generations,” 33% of Gen Xers were laid off or subjected to a pay cut during the pandemic. This was also true for 40% of Millennials, but only 21% of Baby Boomers.

Furthermore, the report says, “Since the beginning of the pandemic, two in 10 [Gen Xers] experienced changes to their living situation—with a housing change being more common for younger people. Debt is complicating the finances of 35% of Gen Xers—higher than the rates of Boomers and the Silent Generation.” (The Silent Generation is the demographic that precedes Baby Boomers, roughly those born between 1928 to 1945.)

Given the findings of the troubles facing Gen X, the American Institute of Certified Public Accountants (AICPA)’s National CPA Financial Literacy Commission recommends three steps that Gen Xers can take to begin alleviating financial stress. The first is to embrace the idea that while markets go down in the short term, they also go up in the long term. Building a solid financial plan, with the help of an adviser or perhaps a digital financial planning service, can help Gen Xers manage this anxiety.

The second thing the AICPA recommends is taking an honest inventory of one’s finances—including spending habits, debt levels, the interest rates being paid on each type of debt, credit reports and scores, and cash flow. This can help a person see more clearly where they can cut expenses and increase savings.

Thirdly, the AICPA says it is helpful to set up automatic savings plans and to use modern financial tools and apps.

Gen X is the now firmly the “sandwich generation,” says Edward Chairvolotti, CEO of Chairvolotti Financial in Winter Park, Florida. “They are taking care of their children and, in many cases, their parents. Life is busy for them, and it is unfortunate that many incorrectly view retirement as being in the far future.”

Ryan McPherson, director of coaching and financial education at SmartPath in Atlanta, agrees that Gen Xers are “sandwiched” by competing financial priorities.

“For years, Gen X has been conducting the great financial balancing act,” he says. “They are caring for aging parents while handling their own financial goals and challenges. COVID-19 didn’t make this any easier.”

Dan Keady, a chief financial planning strategist at TIAA, agrees with Chairvolotti that, even before the pandemic, Gen Xers were being pulled between their children’s and their parents’ needs. On top of this, he points out, many Gen Xers are saddled with student loan debt.

One of the most effective ways a retirement plan adviser can support members of this generation is to help them pause and take stock of their financial health—and to show them their retirement income projections, Keady says.

“According to our own survey data, only 40% of employees are doing financial planning that looks beyond one year in the future,” he notes. “What I have seen from our surveys, and as a practitioner, is once a person gets their retirement income projection, they can see if they are on track. Most retirement planning tools can then show them that if they invested just a little more, how much more improved their outlook would be. Between the ages of 41 and 56, you still have time to make small changes that could really grow your money.”

It is also important for advisers to realize that during the pandemic lockdowns when people were staying at home, many were not spending as much money, so Gen Xers might be able to perpetuate the savings habits they have learned over the past year and a half, Keady points out.

“It is important for advisers to help Gen Xers get a kick start, especially if they had to reduce their savings because they were laid off. We used to call this ‘finding coins in your sofa,’” he says. “Advisers can also remind people about the incredible value of deferring enough money in their retirement plan to meet their employer’s match. Another tool that many people aren’t aware of at work is the health savings account [HSA] that may be available to them. Access to an HSA could greatly magnify their tax-free savings.”