For more stories like this, sign up for the PLANADVISERdash daily newsletter.

Data & Research January 27, 2021

Pandemic Lessons: The Importance of the Savings Hierarchy

Sources agree that, without a solid foundation of advice about the ‘savings hierarchy,’ even successful investors can find themselves short of liquidity at critical times, most notably during emergencies.

Reported by

John Manganaro

Laura Varas, Hearts & Wallets founder and CEO, is not shy about diagnosing some of the biggest hurdles facing financial advisory firms and asset managers today.

In her view—which is far from unique—the entire financial services industry would benefit from a fundamental reimagining of the way its goods and services are presented to and consumed by the mass working public. Simply put, the industry’s default mode of product presentation is almost entirely dominated by complex jargon and by discussions of “style boxes,” “factors,” “alpha,” and other sophisticated concepts that relatively few people outside the professional investing community understand.

Drawing on her background working on consumer packaged goods (toothpaste was her specialty), Varas proposes that investment service providers should focus on more concrete and comprehensible issues. A good place to start, in her estimation, is to refocus the consumer experience on the “savings hierarchy.” This is to say, it is important to present consumers with a broad spectrum of easy-to-understand financial products that are built to work together to solve the specific needs individuals face, including short-, medium- and long-term considerations.

A Consumer-Based Approach

It is no surprise to hear this sentiment from Varas, given that her firm’s role in the financial services ecosystem is, as she puts it, to “make it easier for innovators to reimagine their solutions in the context of what consumers need and are actually doing.” She also draws on her ongoing personal experience of facing college education expenses without necessarily having a rational financial plan to meet them.

“I run a financial services company and I will freely admit that I have made mistakes because of the complexity of the system and how difficult it is to match your goals to your consumer decisions,” Varas says. “Personally, I have oversaved in my 401(k) plan and I’ve neglected to invest for my children’s college expenses. I’ve actually had to take unqualified withdrawals and pay horrendous taxes to meet these expenses. These are the issues I’m talking about.”

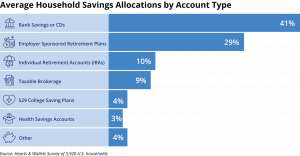

Varas points to Hearts & Wallets data, drawn from a recent survey of nearly 6,000 consumers, showing many savers are missing out by allocating their assets on either end of the liquidity spectrum and skipping the middle. As shown in the chart below, the average U.S. household allocates most of its savings to either end of the liquidity spectrum, with 41% going to “bank savings accounts or certificates of deposit.” On the other hand, 29% goes to employer-sponsored retirement plans such as 401(k)s, 403(b)s and 457s.

“The gap in the middle of the liquidity spectrum includes taxable brokerage, health savings accounts [HSAs], individual retirement accounts [IRAs] and 529s,” Varas says. “These are accounts used by experienced investors to compound wealth for various purposes throughout their working careers and then for retirement.”

The data shows that households that consider themselves “very experienced” with investing send 50% of their savings to the ends of the liquidity spectrum, with the other 50% going to account types in the middle.

“Where to allocate savings is critical to building future wealth,” adds Amber Katris, a Hearts & Wallets subject matter expert. “Experienced investors use the full spectrum of liquidity, compounding wealth and increasing access to funds. Aspiring savers may also benefit from advice to understand how insurance can lessen their perceived need for holding cash deposits, allowing them to invest and benefit longer term in the markets.”

Varas notes that other research conducted by Hearts & Wallets shows a wide disparity in the quality of “savings hierarchy” advice capabilities among the leading U.S. advisory, insurance and brokerage firms. Even those firms that get decent marks on this point—i.e., those that already provide relatively robust advice about how to allocate assets across different account types—could do a lot more to help people meet their goals, Varas says.

Learning From COVID-19

Janus Henderson Retirement Director Ben Rizzuto raises similar points in comments sent to PLANADVISER. In particular, Rizzuto says, the events of the past year have reinforced the importance of being financially prepared for unexpected emergencies and extended periods of work disruption.

“If anything positive came out of 2020, it’s the fact that the challenges we’ve faced over the past year gave us the opportunity to take a step back and consider what is truly important,” he says. “After seeing so many people’s lives turned upside down by the pandemic, many of us have placed a greater focus on our health, priorities and financial stability. As a result, many plan sponsors and business owners have had to reconsider what benefits and savings vehicles their participants and employees need.”

Rizzuto says the cash or cash-equivalent emergency fund is quickly becoming one of the foundational ideas in financial planning, yet it is something very few people take the time to set up and fund.

“In fact, according to the U.S. Federal Reserve, nearly four in 10 American households cannot come up with $400 in a financial emergency,” Rizzuto says, citing the commonly repeated fact. “This startling statistic—along with the economic turmoil the coronavirus pandemic continues to impart on businesses—has caused more plan sponsors and businesses to think about how to help employees put money into an emergency fund. Employers are in the perfect position to do this since their payroll systems can easily link to retirement plan savings options or options outside the plan.”

Echoing comments made by Varas, Rizzuto concludes that behavioral nudges are important to get investors focused on the “savings hierarchy.”

“These nudges help to remind participants what is available and allow a company’s benefits team to have a conversation with employees, so they can make the best decision possible,” he says.