Never miss a story — sign up for PLANADVISER newsletters to keep up on the latest retirement plan adviser news.

Data & Research September 27, 2022

Analysis of American Workers Shows Retirement Plan Type Influences Spending Habits

A study of government employees reported that those with defined benefit retirement plans typically spend a higher percentage of their income than those with a defined contribution or hybrid plan.

Reported by

Paul Mulholland

A new report by the Public Retirement Research Lab and JP Morgan demonstrated that public-sector workers whose primary retirement account is a defined benefit account tend to spend a higher ratio of their earnings than those with a defined contribution account.

The PRRL is a collaboration of the Employee Benefit Research Institute and National Association of Government Defined Contribution Administrators. They combined their datasets on public employees with defined contribution, defined benefit, and hybrid plans with JP Morgan’s data on their customer’s income and savings collected by monitoring cash flows in and out of their JP Morgan accounts.

When they limited their combined data to household participants aged 25 to 64, so they could focus in on those of working age, they ended up with 36,690 households. Members of the household measured had to have a JP Morgan bank account to be included in the study, so if one member of the household had an account, but other members banked elsewhere, the total household size would be counted as one.

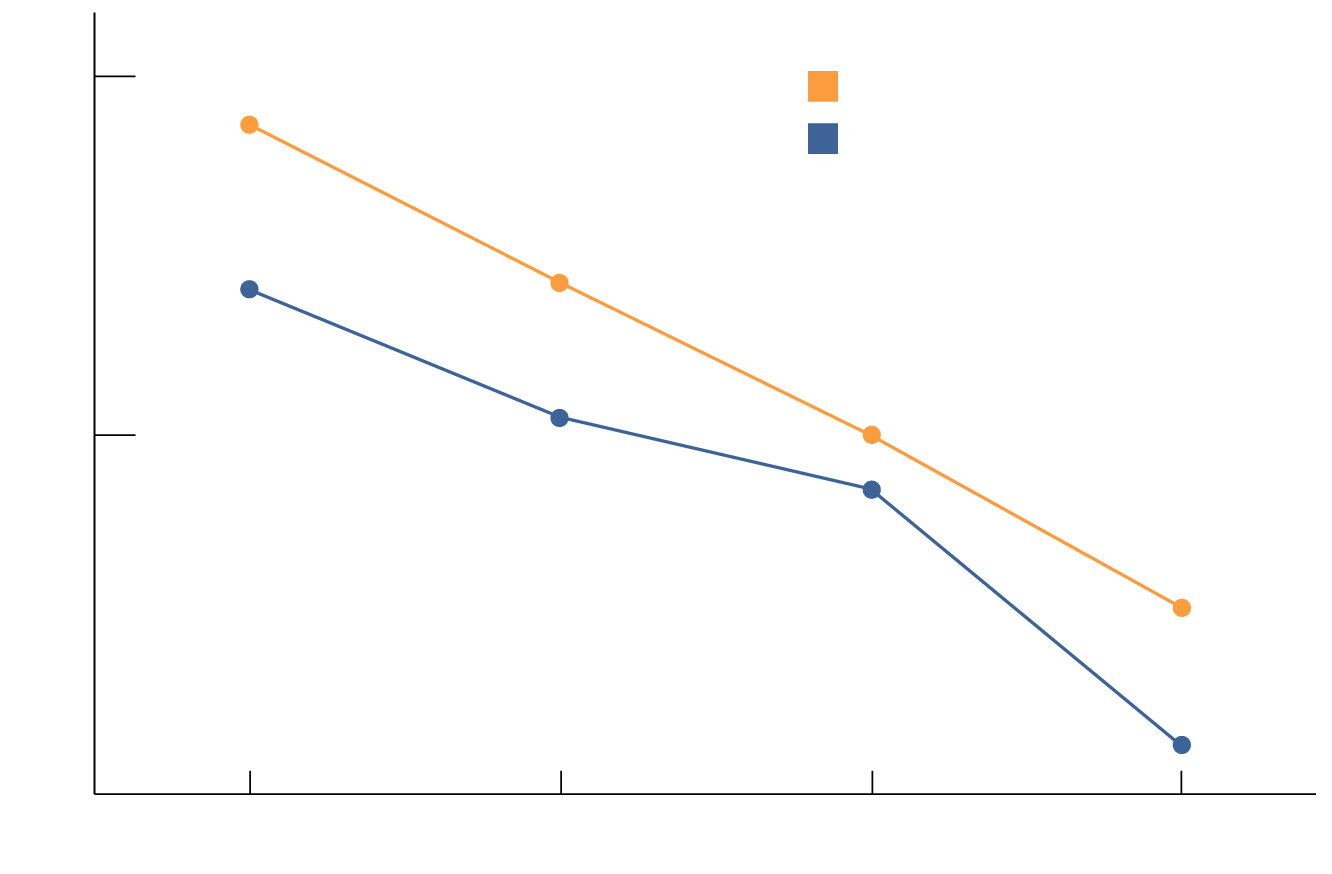

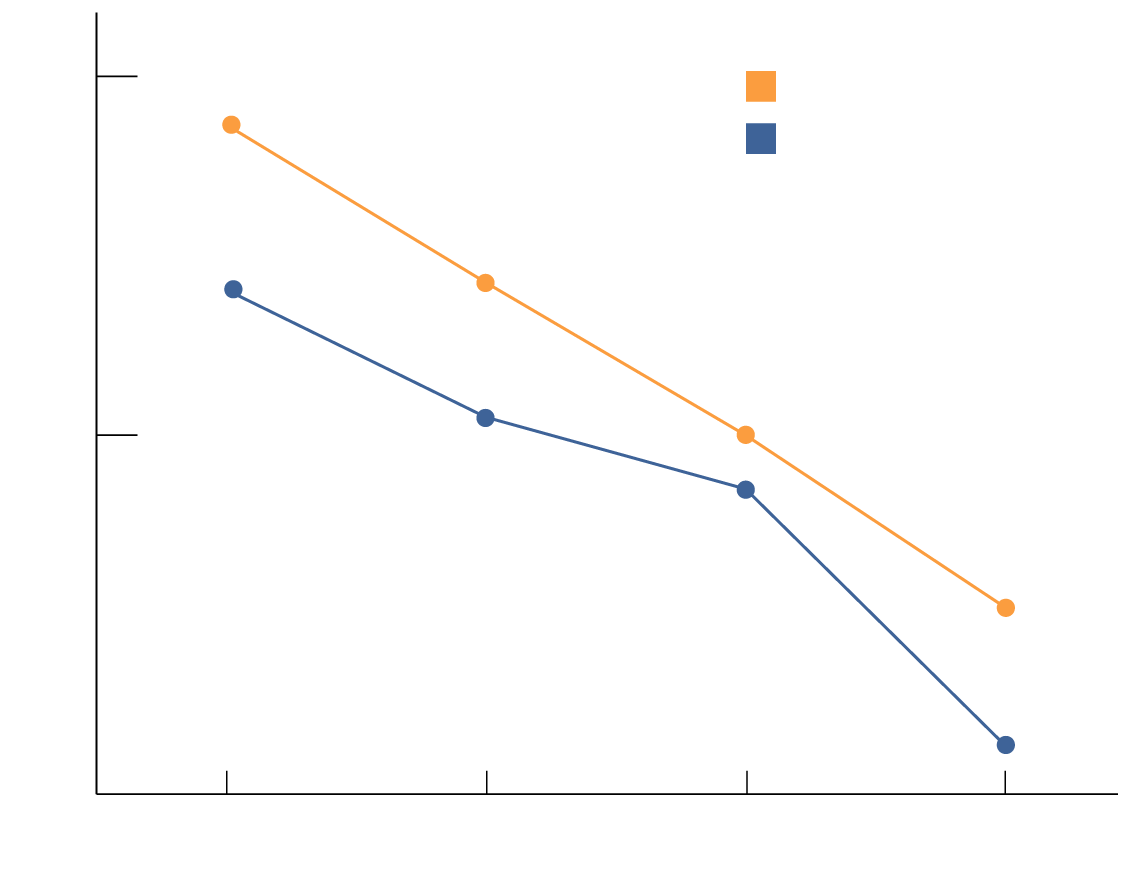

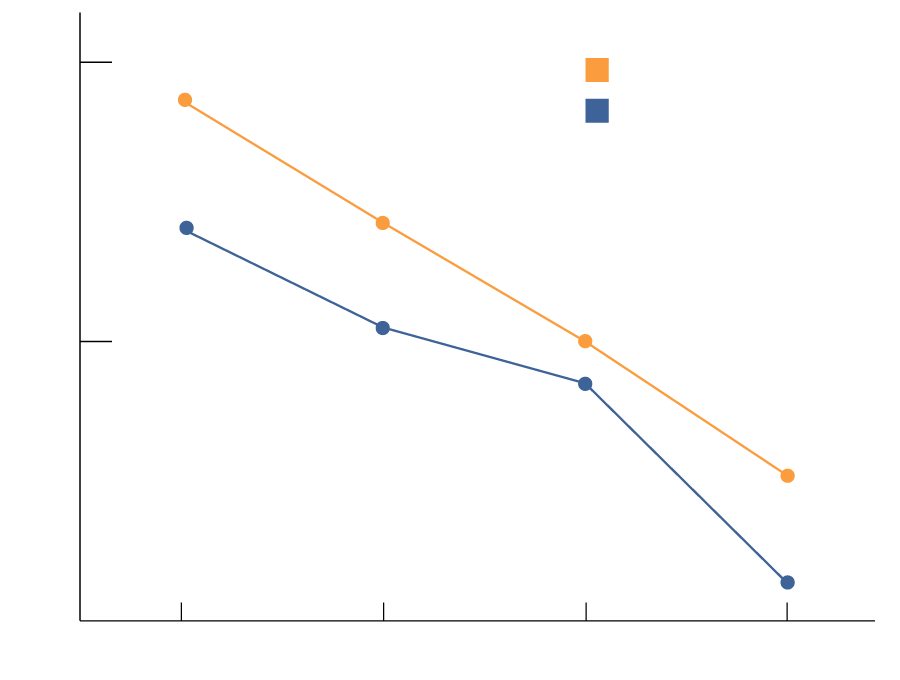

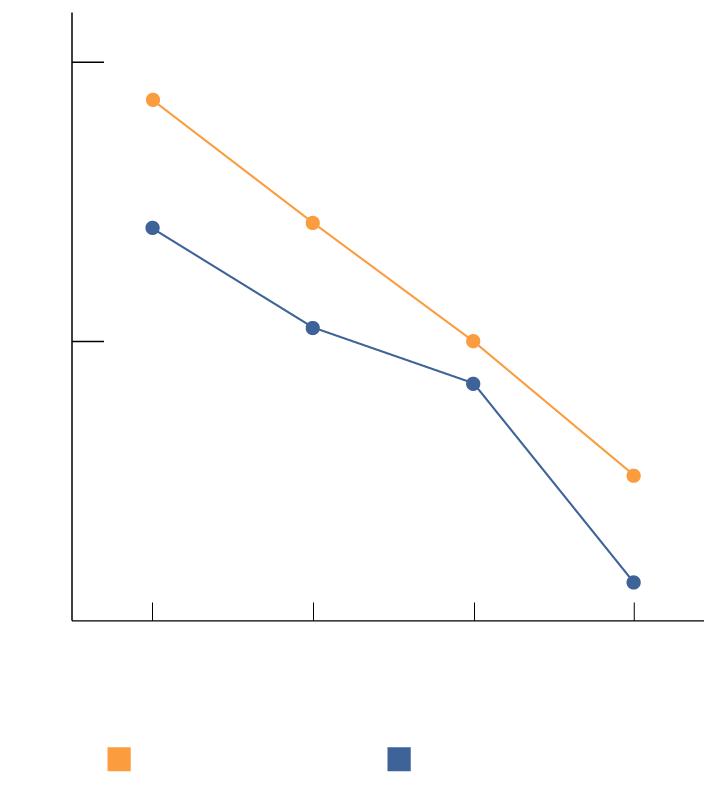

The study, written by Craig Copeland of EBRI; Kelly Hahn, of J.P. Morgan Asset Management; and Matt Petersen of NAGDCA, found that across all income quartiles, defined benefit plan participants spend a higher ratio of their income than defined contribution or hybrid plans. At the lowest quartile, defined benefit participants spent 117% of their income vs 108% for non-defined benefit, and at the highest quartile, defined benefit participants spent 90%, vs 83% for non-defined benefit participants.

Spending-to-Net-Income Ratio, by Income and Primary Defined Benefit (DB) Status

120

Primary DB

117.3%

Primary Non-DB

108.5%

108.1%

100.0%

100

101.0%

97.0%

90.4%

82.7%

80

Lowest Quartel

2nd Quartel

3rd Quartel

Highest Quartel

120

Primary DB

117.3%

Primary Non-DB

108.5%

108.1%

100.0%

100

101.0%

97.0%

90.4%

82.7%

80

Lowest Quartel

2nd Quartel

3rd Quartel

Highest Quartel

120

Primary DB

117.3%

Primary Non-DB

108.5%

108.1%

100.0%

100

101.0%

97.0%

90.4%

82.7%

80

Lowest Quartel

2nd Quartel

3rd Quartel

Highest Quartel

120

117.3%

108.1%

108.5%

100.0%

100

101.0%

97.0%

90.4%

82.7%

80

Lowest

Quartel

2nd

Quartel

3rd

Quartel

Highest

Quartel

Primary Non-DB

Primary DB

Source: PRRL Database and Select Chase Data

The authors speculated that this gap is likely because workers with a defined benefit plan have a retirement that is based on a formula, rather than market performance, and is perceived as lower risk. This reduced risk makes them feel more comfortable spending larger percentages of their total income.

The study found essentially no differences in the spending habits between the two categories concerning what they spent their money on exactly. However, since spending data came from bank account usage, the researchers do not know what cash and checks were spent on.

Additionally, the study noted that some state and local government employers are exempt from Social Security if they offer a retirement plan that is at least as generous as Social Security itself. They tested if Social Security coverage affected worker spending between the two categories, and found that it did not.

The main finding of the study was that public-sector employees who have a defined benefit pension fund tend to spend a higher ratio of their total earnings than their non-defined benefit counterparts.