Never miss a story — sign up for PLANADVISER newsletters to keep up on the latest retirement plan adviser news.

Thought Leadership August 3, 2018

Two Key Themes for DC Plans

For defined contribution (DC) plan participants, wealth accumulation has depended on both equities and fixed income. Yet fixed income will be ever more important in 2018 and beyond, in our view.

Sponsored by

PIMCO

Richard Fulford, Executive Vice President, Head of U.S. Retirement at PIMCO

Here are some suggestions for adapting DC menus to better serve participants in the years ahead.

TDFs: Go Active Where It Matters, Passive Where It Saves

Target-date funds (TDFs) offer participants a diversified, all-in-one default solution for potential wealth accumulation. But TDFs, which entered the scene nearly 25 years ago, need optimization along the active-passive axis. In our view, sponsors may improve participant outcomes and prudently manage plan expenses by employing active and passive strategies selectively.Today, 98% of DC plan sponsors that use TDFs have underlying strategies that are exclusively passive or exclusively active, according to BrightScope. Only 2% of plan sponsors use TDFs that blend active and passive approaches.

In contrast, 62% of plan sponsors blend active and passive approaches on the core menu.

Why the inconsistency? We suspect this is due, at least in part, to a dearth of active/passive blend TDF strategies. Over time, however, we expect TDF allocations will migrate to blend strategies, improving alignment with plan sponsor preferences.

A blend approach makes good sense: Go active where it matters, particularly in fixed income, where alpha has been historically more consistent; go passive where it saves, especially in equities, where the cost differential between active and passive is significant, 59 basis points on average.i

Blend TDFs that actively manage bonds and passively manage stocks may not only reduce plan costs, but they also may deliver results that are superior to exclusively active or passive approaches.

We make the case for active fixed income in “Bonds Are Different: Active Versus Passive Management in 12 Points.” Active management has historically been successful in fixed income because, in part, unlike the equity market, the bond market has a variety of structural inefficiencies that active managers can exploit to seek alpha. Data support our view: About 80% of active fixed income managers ii beat their median passive peers over the five years ended 31 December 2017. In contrast, only 37% of active equity managers iii outperformed their median passive peers during the five-year period ended December 2017.

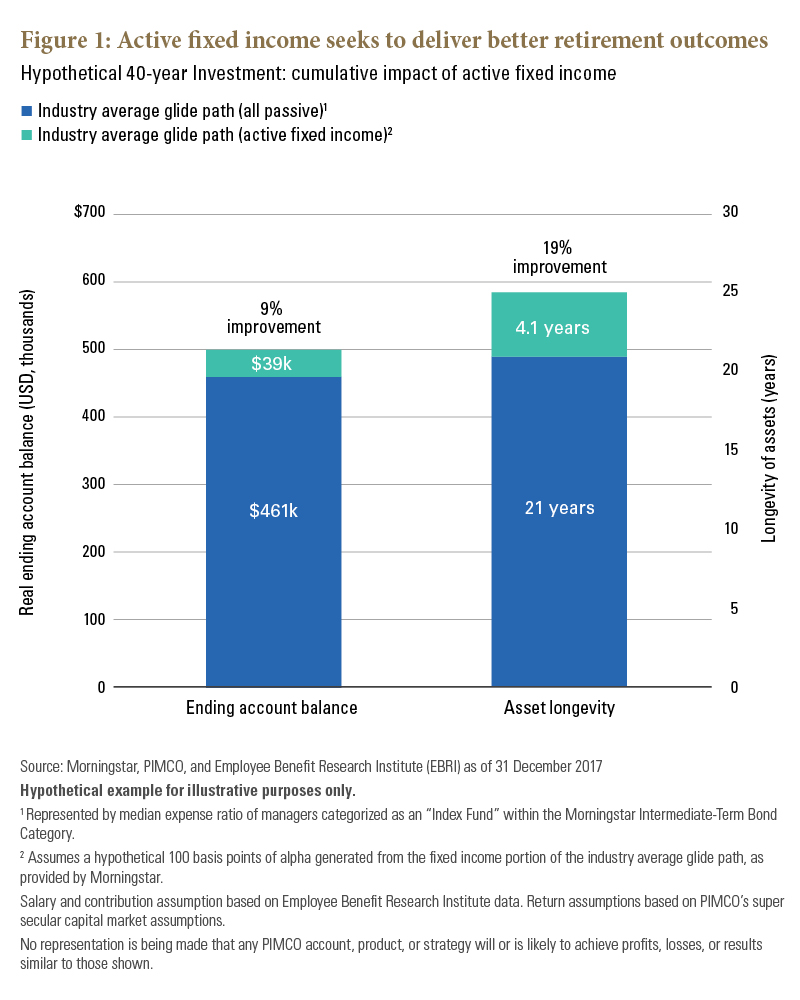

The potential benefits of active fixed income are great. This is most true for individuals who are near or in retirement, when glide path allocations to fixed income peak. For example, a participant invested in the market-average TDF that employs actively managed bonds and generates an additional 100 basis points (bps) of alpha annually on the bond portion of the glide path realizes a dramatic improvement in retirement outcomes over a fully passive approach. Asset longevity jumps by 19% (from 21 to 25 years) and retirement assets increase by 9%. See Figure 1 below.

In short, we believe that qualified default investment alternative (QDIA) strategies that blend active bond investing with passive equity exposure represent the most capital-efficient approach—and can potentially increase the odds that savers reach their retirement objectives.

Retirement Income: Don’t Make Perfect The Enemy of The Good

In theory, a perfect retirement income solution would provide a guaranteed level of lifetime income and an absence of investment risk. In practice, mythical solutions of this sort do not exist, and most retirement solutions that include some form of insurance guarantee are far from perfect. They suffer from complexity, high cost, incremental sponsor risk, and a lack of transparency and transferability. Not surprisingly, adoption of guaranteed solutions by sponsors and participants has been limited.

Surveys show, though, that participants prefer good, if imperfect, solutions. They value low volatility and full control over drawdowns, and prefer to source income from interest and dividend distributions rather than principal. They’re willing to forgo insurance for the absence of the complexity, high cost and other drawbacks noted above.

In practice, of course, participant preferences may vary widely. But momentum to embrace practical solutions appears to be building.

One sign is the surging interest among plan sponsors to retain plan participants after they retire. According to the 2018 Callan Defined Contribution (DC) Trends Survey, 48% of plan sponsors with a written policy for employee retention seek to retain participants in plan post retirement, up from 28% in 2016. Sponsors see benefit in scaling up assets as a means to reduce fees on behalf of all participants.

We’re also seeing more sponsors reviewing plan structure, including retirement income options. Interest has centered on evaluating risk-managed, market-based solutions that have the potential to convert wealth into steady monthly payouts, provide a measure of principal protection and some assurance of asset longevity, as opposed to insurance guarantees.

PIMCO and others also are calling for the addition of a fourth tier on DC menus for retirement income. This would be an important step forward and spur innovation. In addition, if paired with appropriate participant education and retirement income tools, a fourth tier would provide participants with clarity around investment solutions that are appropriate for the decumulation phase.

i As of 31 December 2017. Based on prospectus net expense ratio of actively-managed funds relative to “Index Fund” strategies, as defined by Morningstar. Average fee premium based on average premium across the fixed income and equity Morningstar categories specified below. Based on Morningstar U.S. ETF and U.S. Open-End Fund Categories (Institutional shares only). Large cap represented by Morningstar U.S. Large Cap Blend category, Small Cap represented by Morningstar U.S. Small Cap Blend category, Global (equities) represented by Morningstar World Equity category, Core represented by Morningstar Intermediate-Term Bond category, High Yield represented by Morningstar U.S. High Yield Bond category, Global (bonds) represented by Morningstar World Bond category.

ii Refers to intermediate-term, global and high yield bonds, three of the largest fixed income categories in DC plans.

iii Refers to large cap, small cap and global, three of the largest equity categories in DC plans.

Past performance is not a guarantee or a reliable indicator of future results. All investments contain risk and may lose value. Investing in the bond market is subject to risks, including market, interest rate, issuer, credit, inflation risk, and liquidity risk. The value of most bonds and bond strategies are impacted by changes in interest rates. Bonds and bond strategies with longer durations tend to be more sensitive and volatile than those with shorter durations; bond prices generally fall as interest rates rise, and the current low interest rate environment increases this risk. Current reductions in bond counterparty capacity may contribute to decreased market liquidity and increased price volatility. Bond investments may be worth more or less than the original cost when redeemed. Equities may decline in value due to both real and perceived general market, economic and industry conditions. Investing in foreign-denominated and/or -domiciled securities may involve heightened risk due to currency fluctuations, and economic and political risks, which may be enhanced in emerging markets. Diversification does not ensure against loss.

Glide Path is the asset allocation within a Target Date Strategy (also known as a Lifecycle or Target Maturity strategy) that adjusts over time as the participant’s age increases and their time horizon to retirement shortens. The basis of the Glide Path is to reduce the portfolio risk as the participant’s time horizon decreases. Typically, younger participants with a longer time horizon to retirement have sufficient time to recover from market losses, their investment risk level is higher, and they are able to make larger contributions (depending on various factors such as salary, savings, account balance, etc.). Generally, older participants and eligible retirees have shorter time horizons to retirement and their investment risk level declines as preserving income wealth becomes more important.

Hypothetical examples are for illustrative purposes only. No representation is being made that any account, product, or strategy will or is likely to achieve profits, losses, or results similar to those shown. Hypothetical or simulated performance results have several inherent limitations. Unlike an actual performance record, simulated results do not represent actual performance and are generally prepared with the benefit of hindsight. There are frequently sharp differences between simulated performance results and the actual results subsequently achieved by any particular account, product or strategy. In addition, since trades have not actually been executed, simulated results cannot account for the impact of certain market risks such as lack of liquidity. There are numerous other factors related to the markets in general or the implementation of any specific investment strategy, which cannot be fully accounted for in the preparation of simulated results and all of which can adversely affect actual results.

Statements concerning financial market trends or portfolio strategies are based on current market conditions, which will fluctuate. There is no guarantee that these investment strategies will work under all market conditions or are suitable for all investors and each investor should evaluate their ability to invest for the long term, especially during periods of downturn in the market. Outlook and strategies are subject to change without notice. Performance results for certain charts and graphs may be limited by date ranges specified on those charts and graphs; different time periods may produce different results.

This material contains the opinions of the manager and such opinions are subject to change without notice. This material has been distributed for informational purposes only and should not be considered as investment advice or a recommendation of any particular security, strategy or investment product. Information contained herein has been obtained from sources believed to be reliable, but not guaranteed. No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission. PIMCO is a trademark of Allianz Asset Management of America L.P. in the United States and throughout the world. Pacific Investment Management LLC, 650 Newport Center Drive, Newport Beach, CA 92660, 800-387-4626. ©2018, PIMCO.

CMR2018-0710-343765