Thought Leadership December 12, 2017

Change Management: The Value of Flexibility

The shifting retirement plan landscape offers advisers a chance to rethink the range of solutions they use with clients.

Sponsored by

Ascensus

Neil Smith

PLANADVISER spoke recently with Neil Smith, executive vice president of corporate strategy at Ascensus, to learn more about what’s changing, how plan advisers can position themselves to succeed, and how Ascensus can help.

PLANADVISER: How are the new fiduciary rule and the resulting focus on value versus fees changing the way retirement plan advisers work with clients?

Neil Smith: It’s no surprise that we’re seeing a fairly significant shift toward more transparent fee-based models in retirement plans. This has been in motion for several years. The shift started with independent RIAs operating on a fee-for-service basis and acknowledging a fiduciary role with their clients. Now, as more wealth management advisers migrate into the retirement space, they’re bringing their traditional fee-based pricing models with them. Without a doubt, the Department of Labor fiduciary regulation has accelerated the change.

PLANADVISER: How are broker-dealers helping advisers adapt to these changes?

Smith: They’re taking a couple of different approaches. In some cases, they’re creating groups of specialist retirement advisers that have met some kind of a qualification level that gives the home office comfort that the adviser will be able to operate under this new regulatory standard. In other cases, we’re seeing home offices developing products with what we’d call “guardrails.” The idea is to allow the broader-based wealth management advisers to offer solutions in which the firm steps into a co-fiduciary role and develop products that ensure that core services are uniformly applied across the client base.

PLANADVISER: Can you elaborate on how that works in practice?

Smith: With these solutions, firms want to ensure that advisers are executing against the regulations and the client’s needs in a way that protects the interests of the advisers, the firm, and the client. In a typical example, the home office will step in as a co-fiduciary on the investment platform. The home office or another designated fiduciary is creating the menu and, as a provider, Ascensus is supporting their needs with our integrated tools and technology. They also will look at additional product features—managed accounts for example—that may assist advisors in delivering key services and meeting the plan’s regulatory requirements.

PLANADVISER: What can advisers themselves do to reinforce their value to their clients? Clearly this is more than a matter of changing the way they bill for their services or introducing a new product.

Smith: Advisers need to rethink core aspects of their business. We’re encouraging them to revisit their value proposition and to clearly position it with their clients. We also recommend that advisers work to better understand their own P&L statement when it comes to servicing a plan, and how that ties back to their value proposition. Specialists may also choose to provide more of the education and fiduciary services themselves in larger plans, and use products that provide co-fiduciary solutions with smaller plans to build efficiencies in their practice.

PLANADVISER: Should advisers rethink the types of plans they want to work with or how they approach them?

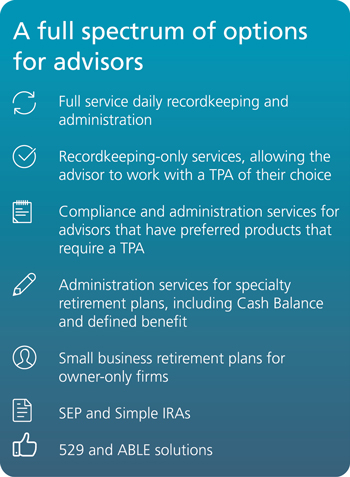

Smith: Advisers need to determine how they want to operate by market segment—takeover plans versus startup plans, for example, or plans that have assets above or below certain thresholds—and how they want to respond to their clients’ needs. At Ascensus, we support a range of solutions that can be tailored to these specific needs. We offer bundled, open-architecture retirement plans, but we also offer a recordkeeping-only solution in which we work with a third-party administrator chosen by the adviser and their client. Or, we can provide third-party administration and compliance services while using another provider’s recordkeeping services.

PLANADVISER: In essence, you’re saying advisers need the flexibility to work with a plan sponsor no matter what that sponsor needs or how it wants to run its plan.

Smith: Exactly—and we think that’s a big deal. If I’m an adviser trying to meet my client’s needs, do I need a bundled solution with a single provider, or do I want to work with a third-party administrator using different provider platforms? The financial adviser should be able to choose what makes sense for them and their clients, given the situation.

PLANADVISER: Is this a good time to be an adviser?

Smith: When things change, some people see opportunities and others see threats. If you haven’t been particularly focused on the retirement space, it creates a new set of challenges. You can probably find turnkey fiduciary solutions that let you continue to have relationships with plan sponsors. And if you’re an adviser who’s doubling down on the retirement marketplace, this is an opportunity to continue growing your business using a model you’ve probably been using for years—which puts you ahead of the curve.

PLANADVISER: What is Ascensus doing to help plan advisers navigate these changes? How does your business model help them?

Smith: Ascensus is and always has been adviser-centric. We only service plans through the trusted relationship of the financial adviser.

Because we’ve been in the fee-based marketplace for over 10 years, we have a very knowledgeable and experienced sales team that helps our advisers move to more transparent solutions. We can deconstruct fees across providers, investment managers, and advisers. In addition, we can give advisers tools that help them explain all of this in an easy-to-understand manner for their clients.

Most importantly, we offer a broad range of solutions that allow financial advisers to choose how they want to work with their clients—with emphasis on the word their. We believe that advisers should have access to solutions that their clients need, not products that someone else needs them to sell. At Ascensus, we’re agnostic to the specific products and business partners an adviser wants to use. We just want to offer them the right solution.

Bottom line, the adviser and the client get to choose what will work best for them.

Visit alwayshaveaplan.com for more information.

Sponsored by

« Movers & Shakers: Ryan Tiernan Vice President, National Accounts, American Funds® from Capital Group